0

Comments

If you’re self-employed and don’t have withholding from paychecks, you probably have to make estimated tax payments. These payments must be sent to the IRS on a quarterly basis. The third 2019 estimated tax payment deadline for individuals is Monday, September 16. Even if you do have some withholding from paychecks or payments you receive, you may still have to make estimated payments if you receive other types of income such as Social Security, prizes, rent, interest, and dividends.

Read More

It’s not just businesses that can deduct vehicle-related expenses. Individuals also can deduct them in certain circumstances. Unfortunately, the Tax Cuts and Jobs Act (TCJA) might reduce your deduction compared to what you claimed on your 2017 return.

Read More

Incentive stock options (ISOs) are a popular form of compensation for executives and other employees of corporations. They allow you to buy company stock in the future at a fixed price equal to or greater than the stock’s fair market value on the ISO grant date. If the stock appreciates, you can buy shares at a price below what they’re then trading for. But careful tax planning is required because of the complex rules that apply.

Read More

Working from home has become commonplace. But just because you have a home office space doesn’t mean you can deduct expenses associated with it. And for 2018, even fewer taxpayers will be eligible for a home office deduction.

Changes under the TCJA

For employees, home office expenses are a miscellaneous itemized deduction. For 2017, this means you’ll enjoy a tax benefit only if these expenses plus your other miscellaneous itemized expenses (such as unreimbursed work-related travel, certain professional fees and investment expenses) exceed 2% of your adjusted gross income.

For 2018 through 2025, this means that, if you’re an employee, you won’t be able to deduct any home office expenses. Why? The Tax Cuts and Jobs Act (TCJA) suspends miscellaneous itemized deductions subject to the 2% floor for this period.

If, however, you’re self-employed, you can deduct eligible home office expenses against your self-employment income. Therefore, the deduction will still be available to you for 2018 through 2025.

Other eligibility requirements

If you’re an employee, your use of your home office must be for your employer’s convenience, not just your own. If you’re self-employed, generally your home office must be your principal place of business, though there are exceptions.

Whether you’re an employee or self-employed, the space must be used regularly (not just occasionally) and exclusively for business purposes. If, for example, your home office is also a guest bedroom or your children do their homework there, you can’t deduct the expenses associated with that space.

2 deduction options

If you’re eligible, the home office deduction can be a valuable tax break. You have two options for the deduction:

More rules and limits

Be aware that we’ve covered only a few of the rules and limits here. If you think you may be eligible for the home office deduction on your 2017 return or would like to know if there’s anything additional you need to do to be eligible on your 2018 return, contact us.

If you’re an executive or other key employee, you might be rewarded for your contributions to your company’s success with compensation such as restricted stock, stock options or nonqualified deferred compensation (NQDC). Tax planning for these forms of “exec comp,” however, is generally more complicated than for salaries, bonuses and traditional employee benefits.

And planning gets even more complicated if you could potentially be subject to two taxes under the Affordable Care Act (ACA): 1) the additional 0.9% Medicare tax, and 2) the net investment income tax (NIIT). These taxes apply when certain income exceeds the applicable threshold: $250,000 for married filing jointly, $125,000 for married filing separately, and $200,000 for other taxpayers.

Additional Medicare tax

The following types of exec comp could be subject to the additional 0.9% Medicare tax if your earned income exceeds the applicable threshold:

NIIT

The following types of gains from stock acquired through exec comp will be included in net investment income and could be subject to the 3.8% NIIT if your modified adjusted gross income (MAGI) exceeds the applicable threshold:

Keep in mind that the additional Medicare tax and the NIIT could possibly be eliminated under tax reform or ACA-related legislation. If you’re concerned about how your exec comp will be taxed, please contact us. We can help you assess the potential tax impact and implement strategies to reduce it.

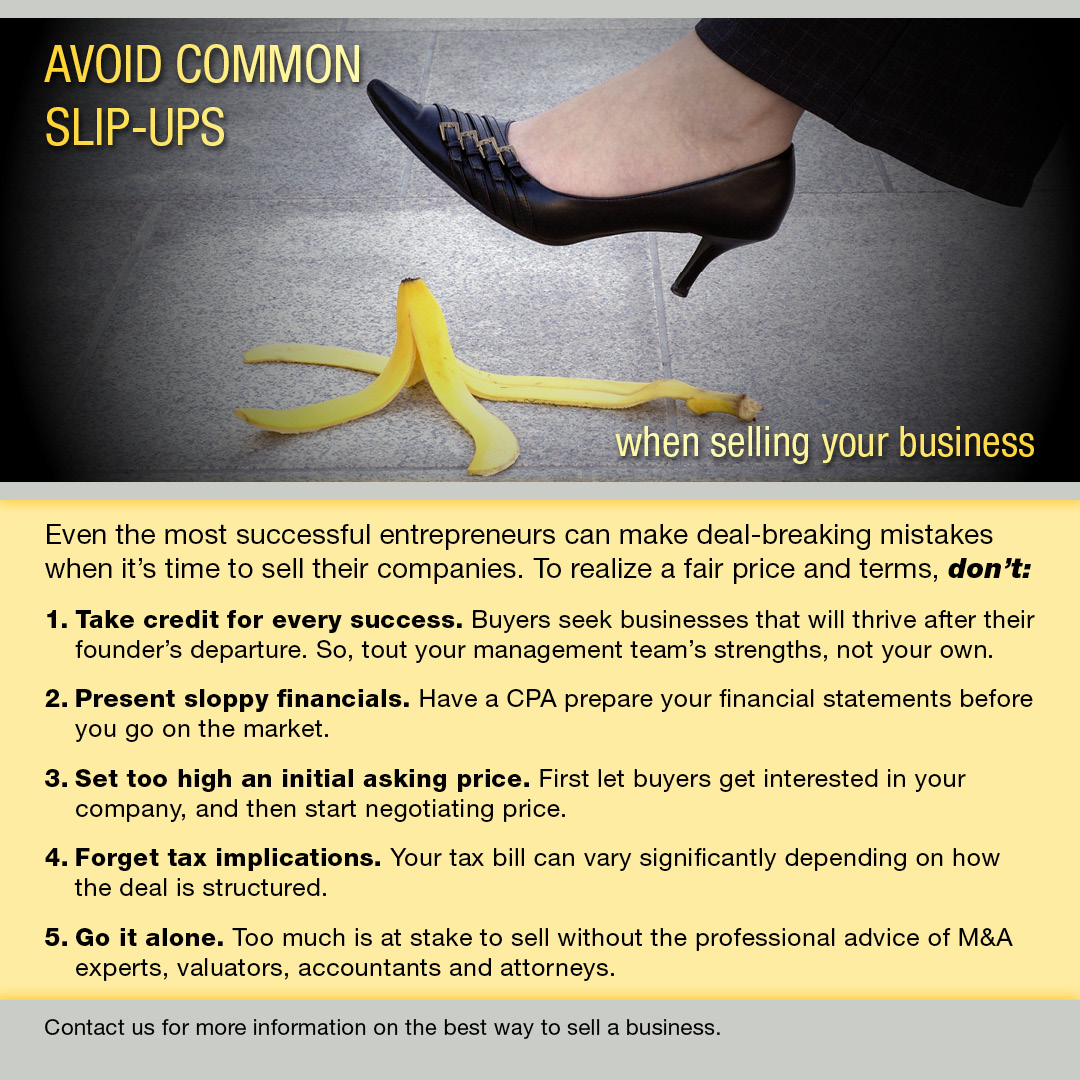

Many small business owners wait too long to prepare their business for sale and consequently leave money on the table when selling. Some owners never plan to sell and others simply get caught off guard by an unexpected illness or unfortunate event. It is best to start preparing your business for sale as soon as possible. Here are several tips to help you increase the value of your business over the next year or two.

Many clients are concerned about “red flags” that can trigger an IRS audit. Since the IRS audits less than one percent of all individual tax returns annually, the odds are pretty low that your return will be chosen for review. I believe that you should take every legitimate deduction that is available to you, so I am not suggesting that you pay more in taxes than you should just to avoid the small risk of a potential audit. That being said, the presence of the following factors in your return increases the chances that the IRS will come calling.